Economic agents face risks of many kinds, which may mutually

covary. A stock broker, for example, is likely to earn a salary

bonus that is positively related to the performance of the stock

market; if that broker also has personal stock investments, his

financial wealth and labor income will be positively correlated.

The first part of this section presents a convenient (and empirically

realistic) formulation in which a consumer faces two shocks (which can

be interpreted as a shock to noncapital income and a shock to the rate

of return) that are distributed according to a multivariate lognormal

that allows for correlation between them. The second part describes a

computationally simple and convenient method for approximating that joint

distribution.

1Theory¶

Consider a consumer who faces both a risk to transitory noncapital income[1]

and a risky log rate-of-return that is affected by following factors: the riskless rate ;

a risk premium ; an additional constant (whose purpose will become clear below); a component

that is linearly related to ; and an independent shock {math}\ShkMeanOneLog_{2} \sim \mathcal{N}(-0.5 \sigma^{2}_{2},\sigma^{2}_{2}):

for some constant . Since is the only component of that covaries with ,

Equation (2) yields a description of the return process

in which the parameter controls the correlation between the

risky log return shock and the risky log labor income shock. If

the processes are independent.

Now we want to find the value of such that the mean risky

return is unaffected by (so that we will be able to

understand clearly the distinct effects of labor income risk, the

independent component of rate-of-return risk , and the

correlation between labor income risk and rate-of-return risk,

). Thus, we want to find the such that

regardless of the values of and . We therefore need:

Using standard facts about lognormals (cf. ), and for convenience

defining , we have

Alternative representation (commented out)

2Computation¶

A key step in the computational solution of any model with uncertainty is the calculation

of expectations. Writing and and , the expectation of some function that depends on the realization of

the risky return and the labor income shock is:

where is the joint cumulative distribution

function. Standard numerical computation software can compute this

double integral, but at such a slow speed as to be almost unusable.

Computation of the expectation can be massively speeded up by

advance construction of a numerical approximation to

.

Such approximations generally take the approach of replacing the distribution function

with a discretized approximation to it; appropriate weights are attached to

each of a finite set of points indexed by and , and

the approximation to the integral is given by:

where the and matrices contain the conditional means of the two variables in each of the regions. Various methods are used for constructing the weights and the nodes (the and points for

and ).

Perhaps the most popular such method is Gauss-Hermite interpolation (see

Judd (1998) for an exposition, or Kopecky & Suen (2010) for

some alternatives). Here, we will pursue a particularly intuitive

alternative: Equiprobable discretization. In this method, and

boundaries on the joint CDF are determined in such a way as to divide

up the total probability mass into submasses of equal size (each of

which therefore has a mass of ). This is conceptually easier

if we represent the underlying shocks as statistically

independent, as with and above; in that case, each submass is a square region

in the and grid. We then compute the average

value of and conditional on their being

located in each of the subdivisions of the range of the CDF. Since,

in this specification, is a function of , the

values are indexed by both and , but since we have

written as IID, the representation of the approximating

summation is even simpler than (9):

where the function is implicitly defined by (2).

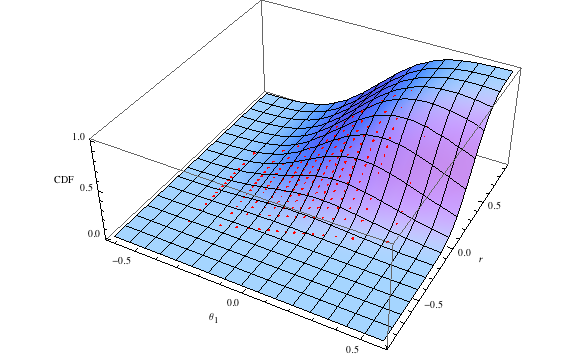

Details can be found in the Mathematica notebook associated with this

section. A particular example, in which and ,

is illustrated in Figure 1; the red dots reflect the height of the approximation

to the CDF above the conditional mean values for and within each of the equiprobable

regions.

Figure 1:‘True’ CDF With Approximation Points in Red for

The assumed distribution has the property , cf. .

An alternative would be to work with and directly, which would require a multivariate normal with nonzero off-diagonal elements (covariances). The two approaches are mathematically indistinguishable, but the IID representation has certain conveniences for our purposes.

- Judd, K. L. (1998). Numerical Methods in Economics. The MIT Press.

- Kopecky, K. A., & Suen, R. M. H. (2010). Finite State Markov-Chain Approximations To Highly Persistent Processes. Review of Economic Dynamics, 13(3), 701–714. 10.1016/j.red.2010.02.002