This section shows how the Envelope theorem is used to derive the consumption Euler equation in a multiperiod optimization problem with geometric discounting and intertemporally separable utility.

The consumer’s goal from the perspective of date t is to maximize the sum of discounted utilities, where geometric discounting means that utility n periods in the future is weighted by βn:

where the derivative dmt+1/dct=−R follows from (2). We can define a function ct(m) that returns the ct that solves the max problem for any given mt. That is, for ct=ct(mt) the first order condition (4) will hold so that

Here’s the key insight: The assumption that consumers are optimizing means that we will always be evaluating the value function and its derivatives at a ct that satisfies the first-order optimality condition (5) (this reasoning would need modification if a liquidity constraint were binding). Thus we have from (7) that

The general principle can be condensed into a rule of thumb by realizing that the Envelope theorem will always imply that the total derivative of a value function with respect to any choice variable must be equal to zero for optimizing consumers (because the first order condition holds). Thus we could have obtained the result immediately by treating ct as though it were a constant (that is, treating the problem as though ct′(mt)=0) and taking the derivative of Bellman’s equation with respect to mt directly. This leads immediately to the key result:

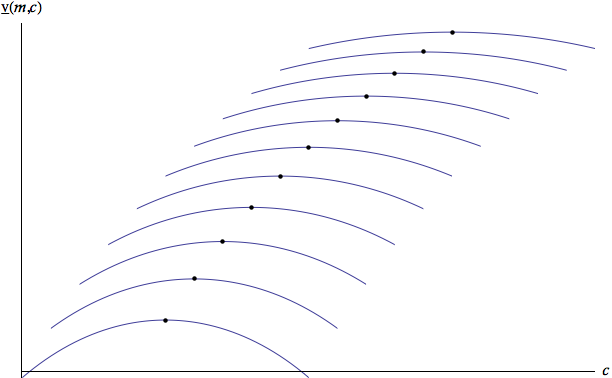

Figure 1:Illustration of the Envelope Theorem at Alternative Values of m

The figure illustrates why the Envelope theorem works: when m increases, the increase in attainable utility is approximately the same whether the extra resources are consumed immediately or saved entirely. This is precisely because the first-order condition equates the marginal utility of consumption to the marginal value of saving, so at the optimum the consumer is indifferent at the margin between these alternatives.